Travel Hacking 101-A Beginner’s Guide to Points and Miles

Have you ever wondered how people fly in business class for the price of an economy ticket, or sometimes even free? What about staying a week at an all-inclusive resort or overwater bungalow for free? You’re in the right place! Travel hacking is the art of using points, miles, and loyalty programs to unlock incredible travel opportunities without draining your wallet.

This beginner-friendly guide will walk you through everything you need to know, from earning points to choosing the right credit card strategy. By the end, you’ll have the tools to start planning your first points-funded trip!

Table of Contents

Credit Card Points and Miles

At the heart of travel hacking are credit card rewards programs. Banks and airlines want your loyalty, so they offer incentives to keep you using their cards. The more you swipe, the more you earn. But it’s not just about spending, sign-up bonuses, transfer partners, and category multipliers are where the real magic happens.

Think of points and miles like a second currency. When used strategically, they can pay for flights, hotels, rental cars, and even once-in-a-lifetime experiences like an overwater villa in the Maldives or a lie-flat seat at 35,000 feet.

What Are Points and Miles

Points and miles are reward currencies issued by banks, airlines, and hotel chains. While the terms are often used interchangeably, there are slight differences:

- Points are usually tied to flexible bank programs (like Chase Ultimate Rewards or American Express Membership Rewards). They can transfer to multiple partners, giving you several redemption options.

- Miles are most often tied to a specific airline’s loyalty program (like American Airlines AAdvantage or United MileagePlus). These are best used for flights within that airline or its alliance partners.

The value of a point or mile depends on how you redeem it. For example, using 60,000 points for a $600 gift card equals 1 cent per point. But transferring those same points to an airline could get you a $2,000 business-class ticket, which makes your points worth 3 cents each!

How are Points and Miles Earned

There are several ways to earn rewards, but credit card sign-up bonuses and spending categories are the fastest routes:

- Sign-up bonuses – New cards often come with 50,000 to 100,000 points when you meet a minimum spend in the first 3 months. That’s often enough for a free round-trip ticket to Europe.

- Category spending – Some cards earn bonus points for specific purchases like dining, travel, or groceries.

- Everyday purchases – Gas, bills, subscriptions, and even taxes can be paid with a credit card. If you’re going to spend the money anyway, you may as well earn rewards.

- Referral bonuses – Many cards offer points for referring friends or family. Keep reading to see how to do this with your P2!

- Shopping portals and promotions – Airlines and banks have portals that let you earn extra points when you shop online through their links. Check out the best shopping portals I use to earn more!

Once you start layering these methods, your points balance can grow surprisingly fast.

Credit Card Strategies

Jumping into travel hacking without a plan can lead to wasted points or cards that don’t align with your goals. Here are a few strategies for beginners:

- Start with a goal in mind – Do you want free domestic flights, international business class, or luxury hotel stays? The best card depends on your travel goals! You may even want to just test the waters and want to get one free trip to see if this hobby is for you.

- Focus on one program at a time – Spreading points across too many programs makes it harder to book. Stick to one provider (like Chase or Amex) when starting. Both of these have several transfer partners!

- Hit minimum spends wisely – Time your applications around big expenses like insurance, tuition, or holidays. Make sure you can hit the minimum spend before applying!

- Pay in full every month – Travel hacking only works if you avoid credit card interest. Carrying a balance wipes out the value of rewards, unless your card has 0% APY.

How to Double Your Points With a P2

One of the most powerful strategies in travel hacking is using a P2 (Player 2). A P2 is simply your partner, spouse, or even a trusted family member who also opens reward cards, and you travel together!

Here’s how it works:

- You both open cards separately and earn the welcome bonuses.

- You refer each other when new cards are opened to earn referral points.

- You pool points (if the program allows it) or book rewards for each other.

For example, let’s say you open the Chase Sapphire Preferred and earn 75,000 points. Your P2 does the same, but you also get a 15,000 referral bonus, and now you have 165,000 points together, enough for two business class flights to Japan from the US, with some left over!

Travel hacking with a P2 accelerates your earnings without doubling your spending.

Travel Reward Credit Cards

Not all credit cards are created equal. Some cards focus on airline miles, some on hotel points, and others on flexible currencies. For beginners, flexible points cards are the best starting point because they give you multiple redemption options.

The most popular transferable travel rewards programs include:

- Chase Ultimate Rewards

- American Express Membership Rewards

- Capital One Miles

- Citi ThankYou Points

Each program has unique transfer partners, so your ideal card depends on which airlines and hotels you value most.

Co-branded vs Transferable Credit Cards

When picking cards, you’ll come across two main types:

- Cobranded cards – Issued in partnership with an airline or hotel. For example, the Citi Platinum AAdvantage card will earn American Airlines miles, and the Amex Marriott Bonvoy Bevy card will only earn Marriott points. These are great if you’re loyal to one brand or want status with a brand.

- Transferable points cards – These cards are issued by banks like Chase, Capital One, or Amex, where points can transfer to multiple airlines or hotels. For example, the Chase Sapphire Preferred Card will earn Ultimate Reward points, and the Capital One Venture will earn Capital One miles. Both of these can transfer to certain airlines and hotels. These cards give you flexibility and generally higher value.

NEW Signup Bonus of 100,000 Ultimate Reward Points! 👉APPLY HERE!👈

As a beginner, start with transferable points. Once you understand your travel goals, you can add co-branded cards to unlock perks like free checked bags, free night certificates, or elite status boosts.

Transferring to Travel Partners

The most valuable redemptions come from transferring points to travel partners. Your transferable point cards all have travel partners you can transfer to. Instead of booking through their bank portal, you move your points to an airline or hotel program where they can stretch further.

For example:

- 35,000 Chase Ultimate Rewards transferred to World of Hyatt can book a night at a luxury all-inclusive hotel

- 70,000 Amex Membership Rewards transferred to Delta Airlines can book round-trip tickets to Europe

- 75,000 Capital One miles transferred to Virgin Atlantic can book a business-class ticket on ANA from the US to Japan, a ticket that would normally cost $5,000

Transfers are typically 1:1 and often instant, though some programs take a day or two. The key is to have a redemption in mind before transferring, since once points leave the bank, they can’t come back.

Next: Read more about how to Redeem your Chase Ultimate Reward points with Hotels and Airlines

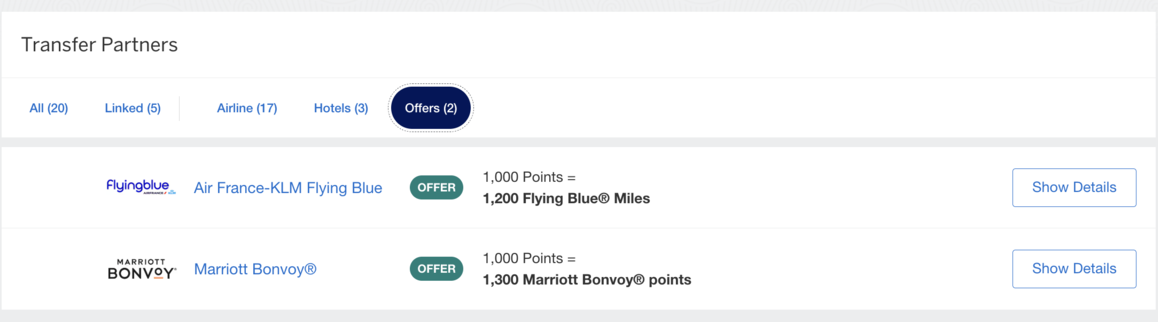

Transfer Bonuses

One thing to keep an eye out for is transfer bonuses. All transferable point programs will occasionally offer this feature, although there’s no fixed schedule for it. New bonuses usually drop every month.

An example of this is when American Express offers a temporary bonus of up to 30% to transfer to Marriott Bonvoy or 20% to Flying Blue, for example. So instead of transferring at a 1:1 ratio, you can transfer 1,000 membership rewards and receive 1,300 Marriott Bonvoy points or 1,200 Flying Blue miles.

It is not wise to speculatively transfer points to another program without a redemption in mind, even if the transfer bonus is over 50%. I say this because programs can devalue at any time, so the points needed for your trip could change. The program could also drop the partner you planned to use, or you may change your own plans and wish you still had the points to transfer somewhere else.

Which Credit Card Should I Start With?

The best starter card depends on your financial situation and travel goals, but here are a few cards I would recommend:

- Chase Sapphire Preferred – My favorite beginner card with a $95 annual fee. A well-rounded card with strong travel protections, 3x points on dining, and access to Chase’s excellent transfer partners.

- Capital One Venture Rewards – Simple earning structure (2x on everything) and flexible redemptions. I call this the “no thinking” card due to no bonus categories to keep track of! Access to Capital One’s transfer partners and a $95 annual fee.

- Chase Freedom Flex – Great no-annual-fee card with rotating bonus categories, cell phone insurance, and best paired with a Sapphire card.

If you’re brand new, the Chase Sapphire Preferred is my favorite beginner card because of its balance of perks, reasonable annual fee, and powerful transfer partners.

NEW Signup Bonus of 100,000 Ultimate Reward Points! 👉APPLY HERE!👈

Business Credit Cards

Don’t overlook business credit cards, you don’t need to own a large company to qualify. Many side hustles, freelance gigs, or even selling items online can count as a business.

Business cards often come with higher welcome bonuses, 0% APR for a limited time, and unique bonus categories. They also don’t show up on your personal credit report (for most banks), which makes it easier to open multiple cards without impacting your credit score as much.

Popular beginner-friendly business cards include:

- Chase Ink Business Preferred – Huge welcome bonus and strong transfer partners.

- Chase Ink Business Cash – No annual fee, high earning rates on office supplies, internet, and phone bills.

- American Express Blue Business Plus – 2x points on all purchases with no annual fee.

Pairing personal and business cards can supercharge your earning potential, and they should be included in your long-term strategy.

FAQ

Will opening several credit cards affect my credit score?

Your credit score is based on several factors, such as the length of your credit history, payment history (making on-time payments), credit utilization (how much of your credit you use), and more. Your score will drop a few points with each card application, but as long as you pay off your statement balance every month and always pay on time, you will see your credit score improve. I recommend using Credit Karma to monitor your score.

Do you keep all your cards open, or do you cancel them?

Always keep your no-annual-fee cards open, even if you don’t use them anymore. If the card does have an annual fee and the benefits are not outweighing the fee, downgrading should be your next option.

How do you keep track of all your credit cards?

I love the TravelFreely app! You don’t have to enter any sensitive information, just card type and date opened, then it tracks all fees and dates, so you don’t have to. You can sign up here!

What is the 5/24 rule?

The Chase 5/24 rule is an unofficial policy that will prevent you from being approved for most Chase credit cards if you have opened five or more personal credit cards in the past 24 months. This rule applies to cards from any issuer, not just Chase. The rule is in place to prevent people from applying for credit cards just for the welcome bonus and then closing the account before the annual fee hits.

Do Points and Miles expire?

Yes, some programs have expiration policies, but activity like earning or redeeming usually resets the clock. Bank points (like Chase Ultimate Rewards) generally do not expire as long as your account is open. As long as you have an open credit line, your points will not expire.

Final Thoughts

Travel hacking might sound complicated at first, but it’s really just a system. You earn points with the right credit cards, you pool them with a partner if possible, and then you redeem them for high-value travel experiences.

The key is to start small, maybe with one flexible rewards card, and build from there. With a little planning, your next vacation could cost a fraction of what you’d normally pay.

If you’ve been dreaming of flying in a lie-flat seat or staying at a luxury resort without the luxury price tag, travel hacking is your ticket.

Next: Check out some of my other Points and Miles posts!